(HYPER) VALUATIONS AND (ZERO) PROFITS: THE FOODTECH TURNING POINT?

“He will win who knows when to fight and when not to fight” Sun Tzu

What “The Art of War” can teach us about investing? According to Sun Tzu, an investment should be done whether there is a clear benefit, after having analyzed deeply the pros and cons, not doing just for the sake of doing something, without getting dragged into the hype.

What follows is a mere list of deals related to global agrifood-tech. Of course no attempt to judge or evaluate them, but simply stating the facts, to understand if global foodtech might have reached a turning point.

A BUNCH OF INTERESTING FACTS AND FIGURES

1st May 2019: Beyond Meat prices its IPO at a price of $25,00$, with an initial market cap of $1,46bn. 3 years later, Beyond Meat reported another slow quarter, with a net revenue of $109,5m (+1,2% YoY), an Ebitda of $-78,9m and some big investors starting to rumble, with the plant-based pioneer facing hurdles.

17th January 2021: Deliveroo closes a Series H round of $180m, bringing the total raised to $1,7bn and reaching a valuation of $7bn. 2 months later, Deliveroo gave London Stock Exchange what has been defined as the “The worst IPO in history”, losing $2,8bn valuation from initial market cap.

19th October 2021: Gorillas closes a Series C round of $1bn, reaching a valuation of $2,1bn. On 23rd May 2002, Gorillas announced 300 layoffs due to internal reorganisation.

17th March 2021: Getir closes a Series E round of $768m, skyrocketing its valuation to $12bn. On 25th May 2022, Getir announced they will reduce the global workforce of 14%, meaning cut off 4’480 employees.

2 years ago, one of the global foodtech rising stars, Zume Pizza, after $423m raised (whose 325 from SoftBank) and $4bn valuation, shifted its business from robotic pizza delivery to food packaging and delivery system. The reasons? Probably we will never know ‘em but it’s hard to not see a connection with profitability.

Impossible Foods raised up to date $2,1bn reaching an undisclosed valuation of $7bn, with a burn rate of $500m per year. Profits? ZERO. Elementary, Watson.

TIME FOR A CHANGE?

Let’s go on with British literature. According to Agatha Christie, one coincidence is just a coincidence, two coincidences are a clue, three coincidences are a proof, so what about four coincidences or more?

Does foodtech have a serious problem with hyper valuation and profitability? Probably there are not enough elements in support of this suggestion and we have to consider that the quick commerce space took advantage of the hype created by the pandemic, which undoubtedly “doped” the numbers. We don’t have to forget that an innovation environment must be, by definition, quick and agile, where startups always keep an eye wide on revenue, keeping closed the eye on profit, but can we affirm that’s definitely time for a change in strategy of foodtech startups?

As per the last report of Dealroom and Five Seasons Venture, funding in the foodtech industry in Q1 2022 dropped 41% from Q4 2021 levels. Are there some first signs of change?

To answer these questions and delineate the next future of global foodtech I reached some reliable international foodtech venture capitalists and experts.

3 simple questions, common for everybody

Do you think it’s time for a less aggressive strategy by foodtech startups or it would alter their innovative spirit, making the rounds less attractive?

Consequently do you think there should be more attention to profit and less to revenues?

Do you think the time of hyper valuation is over so we will see more “smooth” rounds?

DISCLAIMER: The opinions expressed are those of the authors. They do not purport to reflect the opinions or views of the companies they represent, nor they have to be interpreted as a personal judgment about the investment rounds mentioned in the article.

- “This is a quite complex topic, with some substantial differences between Italy and the rest of the world. About the latter, undoubtedly the excess of liquidity and the flattening of other asset classes drove a boom in the valuations, with easy money and crazy cash burn. Something that definitively has to be changed. Conversely, I believe that in Italy the valuations are still at acceptable multiples, and very interesting deals could be made”.

- “Overall yes, but the KPI related to growth will remain the most important metrics to evaluate a project, altough a speed lighting growth may not be always the right choice. It’s self-evident that pushing the revenues to be profitable is always welcome, but it may depend by so many factors. In such an environment, the analysis and due diligence will become ever more important. I want to stress though that personally I value a lot a team that maintains an “every penny counts mentality”, while there are several examples of startups that quickly evolved from penny-pinching to spendthrift. Finally, in a scarcity context, I believe it is more important than ever that investors have a skillset which includes business and management experiences, to provide the founders with a sounding board on the most appropriate burn rate.

- To answer this question I would like to have the crystal ball. As I stated earlier, probably all the markets will slightly go down and this will drive to “smoother” valuations and more “rational” rounds. Neverthless it’s too early to say we are at the end of a cycle, as it depends on so many factors, such as the innovation cycles, the liquidity, the evolution of the geopolitical situation, just to name a few”.

- “I think that it could be suitable to have a top-line growth strategy combined with more attention to the cost base. Another important point is rather how long of a runrate a current investment round creates, where 18-24 months should be the new standard. In my opinion this makes a round attractive. Having a low burn rate and securing multiple investors with deep pockets significantly de-risks the profile of the company.

- “Obviously being profitable from the beginning could sound pretty impossible and unnatural, but I think that reaching the break-even point in 4 / 5 years, say, mid term over long term, is desirable and absolutely feasible with an appropriate strategy. Every startup in the world burns cash, but needless to say there’s a huge difference in burn multiples and burning 100k.

- “Definitely yes, and in this sense we are already watching some corrections in the market. In the last 2 - 3 years some verticals in foodtech, such as quick commerce and even plant-based have been overvalued. A correction was definitely expected and I strongly believe that we are entering in the era of a foodtech more “consciousness and prudence”, with more rational and disciplined valuations.

1. "As you know, we are on the verge of a global economic AND food crisis, that has already started. This will inevitably have an impact on levels of venture capital investments and on valuations. I might be wrong but 2022 is likely not going to be as bright as 2021 in terms of investments in the FoodTech sector. This is still too early to tell, but according to our FoodTech Data Navigator, we are now almost the end of H1 2022 and we have reached only 20% of what was invested in 2021. Some entrepreneurs might still be 'aggressive', but they will quite likely be brought back to market reality by their investors, especially for companies operating in the Food delivery or Plant-based sectors, as you mentioned before. Yet, more than ever, the current situation will contribute to raise awareness of the challenges of our Food System and the solutions that the AgriFoodTech sector can provide"

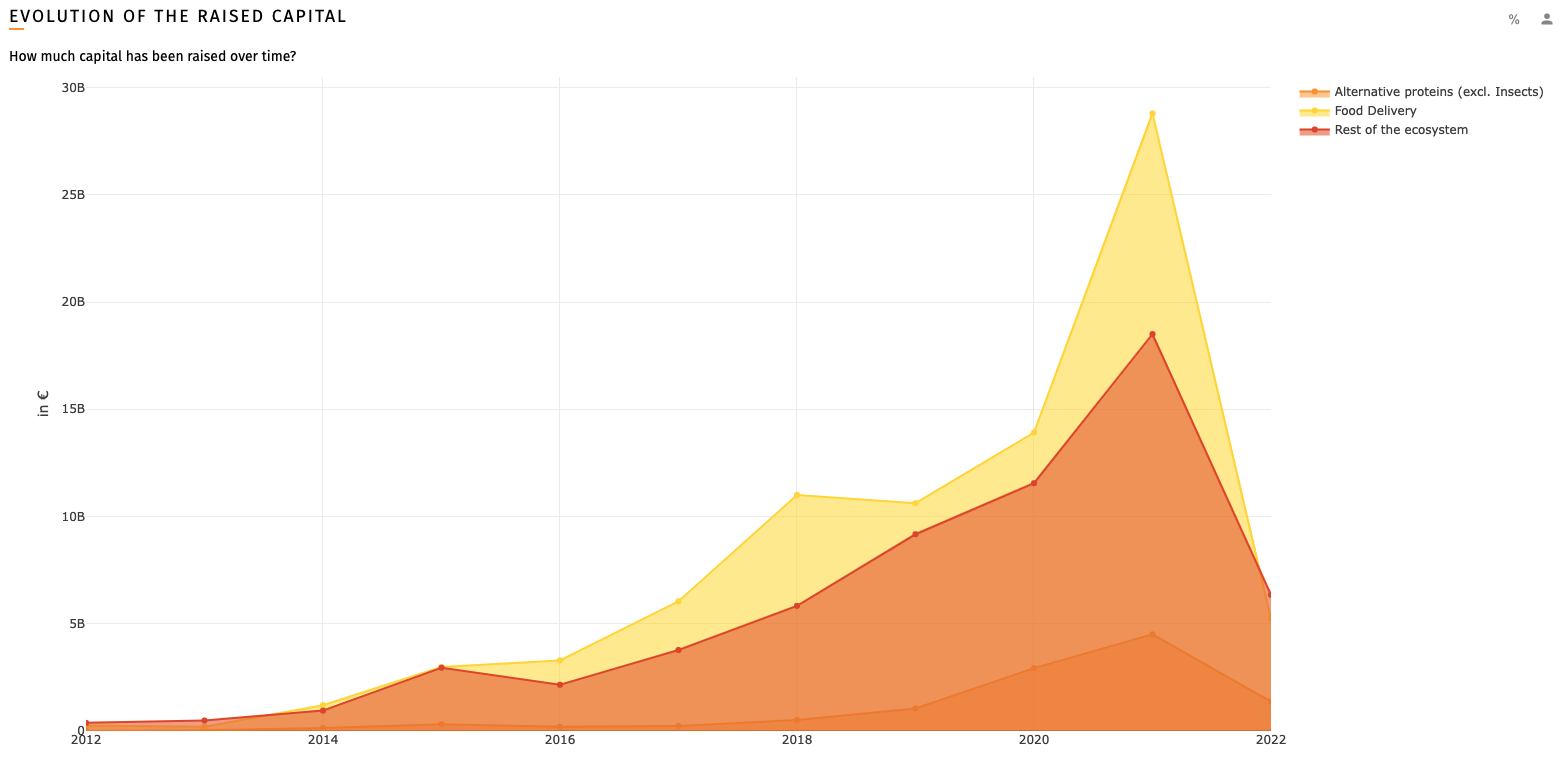

2. "This is a very difficult question as AgriFoodTech is a very broad sector, and many sub-sectors such as cellular agriculture are still pre-revenue and in R&D phase, while attracting large amounts of capital. I think the focus should be on IMPACT. It is time for investors to broaden their scope both in terms of focus areas by embracing a more holistic view of the sector, and broaden their geographical scope, to invest in companies that are ideally financially attractive but are also working on making our Food System more efficient and resilient. Looking at investment data, almost 60% of overall capital invested in FoodTech to date went into food delivery and alternative protein, in 13% of the ecosystem in terms of numbers of companies. The push towards alternative protein should of course continue, but many other areas of AgriFoodtech such as Ag biotech, precision farming, food waste and upcycling technologies, alternative packaging, supply chain traceability technology, are still underfunded, while having the capacity to generate a huge impact.

Source: Forward Fooding FoodTech Data Navigator

3. "I don't know if hyper valuation time is over as it is always about 'cycles', but there will be for sure a 'natural' calibration in the short term. On the positive side, more sensible valuations that more in- line with public-market comparable, also means that not only more investors could enter the market, but it could also perhaps help the existing ones change their focus from 'what is frenzy', to other technologies driving positive change on our Food System. Good news, the AgriFoodTech investors landscape is changing. Over the past couple of years, we have seen a lot more VC emerging, not only with a true knowledge of the sector, but also with a very holistic approach when it comes to their investment thesis, including big players such as Anterra Capital with a recent $260m close, or Synthesis Capital closing an impressive $300M for their first first fund, but also micro-funds such as Trellis Road, proposing a unique approach to investment".

- “There has been much disruption to the global food supply chain in these couple of years. At the same time, there has been continued influx of funding for agritech and food tech startups. I think smart, innovative, and entrepreneurial people will continue to start their own companies to provide solutions to solve some of the problems. However, the market sentiments are more cautious now given the global economic and geopolitical backdrop, and there are many startups seeking funding to boost their liquidity positions.

- “The path to profitability is very important, even in the early stage rounds and it has to be one key metric in the growth process. Consequently, a constant watch on burn rate is mandatory.

- “Of course, nobody has the crystal ball but I can say in the last two years the valuations have been very interesting in some sectors. For example, in the downstream (delivery, quick commerce and so on) experienced huge growth during the pandemic. Another is plant-based alternatives. Valuations had been quite high. . I think that a correction of the market is not unexpected

- "I think many investors have been attracted to FoodTech startups as the potential for disruption on the food value chain has been somehow revealed during the pandemic. This has led to some exuberance, but not to anything close to a bubble. For me, the question about the valuations is not really important, what matters are first the investments that need to be made and second the potential for growth. Let’s be honest, we are talking about huge markets that require also huge investments: grocery retail is a $800B market a year in the US alone, the same in Europe. To take on such a market will require to build an infrastructure in many cities, and may fail. But taking 10% or more of the whole grocery market in these cities could be the foundation of some of the greatest startups ever. I think the reasoning is the same for alternative proteins (a $1,400B market / year globally for animal proteins) and other areas. Hence, I think that if some valuations went overboard, it’s not time to be less agressive, but maybe to be even more so".

- "Yes, but it would mean for investors to be maybe a bit more thorough in

their due diligences when they analyze the path to profitability to some

startups".

- "Yes, for a time at least. However, that also means that the amount

raised by startups will also decrease as funds themselves are raising

less cash and are then dedicating what they still have to the startups

they already have in portfolio".

- “I think the current downturn and reset in valuations is a healthy reality check and readjustment for many foodtech founders, and investors bringing a good dose of reality and significant repricing. I personally, agree with Jessica Pothering’s view expressed on Agfunder who was questioning the current investments in foodtech, and in particular the huge proportion of money allocated in Europe to online egrocery and super-fast delivery, who attracted almost 50% of VC money in Europe, while other companies or sub segments upstream who were doing a better jobs at really solving global issues like climate change, food waste, or removing chemicals and fertilizers from our soils were not getting as much attention and money”.

- " Being profitable allows founders to get more freedom and rely less upon investor’s money, get more power when they need to fundraise as many investors value that some start-ups can run a business profitably, and it offers more exit opportunities. At the same time, start-ups focused on high growth can also get more profit on the long-term. So navigating between growth and profitability will remain a key topic for founders and investors, depending mostly on the sub-sectors, technology, business models and whatever the path chosen, ultimately the key element will be the execution capability of the team to navigate this new uncertain macro trends ( inflation, potential recession) manage cash wisely, raise money when needed, recruit the best talents and build a sustainable company and scale fast. And with the current correction, attention to profitability will definitely becoming increasingly important for investors and founders who will have to be more financially disciplined after years of easy and almost free money as it will be more difficult to raise money for some companies, with the prospect of more down-rounds due to valuation resets".

- "Some of these very high valuations in foodtech resulted initially from a big inflow of capital to the sector which was underfunded for a long time compared to other sectors like biotech or fintech, then the entrance of more corporates, hedge funds, Sovereign funds to the space who led massive rounds in some sub-segments like alternative proteins, indoor ag inflated some of the valuations as the fear of fomo led them often to re-invest massively even when the valuations were very high. This FOMO nurtured this inflation cycle and drove some of these hyper/insane valuations with start-ups rising to stratospheric valuations while being totally disconnected from reality, with unrealistic growth plans and any serious path to profitability. Today the public-market reckoning is causing a total rethink in private markets: tech IPO are pulled out or delayed, entrepreneurs are advised to conserve cash longer and manage their business more efficiently. And VCs are more cautious so we shall see less FOMO and more reasonable rounds in the sector".

- The “hype” of becoming the next Beyond meet is not gone yet. Huge challenges ask for huge solutions. But the “valuation” criteria will adapt as the market is “growing up”. Until now it was all about “revenue”, having the “best (new) innovation/product” out there (exaggerating a bit). Now, other criteria will play a major (new) role for the valuation too. For example, how solid is the company structure / organisation. A good (negative) example is the German food delivery company “Gorilla”. Everyone (investors) loved the business idea. The valuation went through the roof. But Gorilla is now on the brink of failure because their company structure was not set up for their aggressive growth and blew up in their face. Incidents like this will definitely change the (investment) landscape.

- Additionally, there is also a “new generation” of (food) businesses and entrepreneurs emerging, which either rather want to build a solid, profitable “small” family business and are not interested in “scaling” their model but aim to be “THE local hero”. Or, like in other industries, a new generation of B2b suppliers materialize which focus solely on one issue which they solve best, eg. for then many CPG brands. Both need a different kind of investors, “patient capital”, not really the venture Capitalists. VCs must, for satisfying their own investors, be aggressive about the business model, scaling or even having an eye for potential IPOs.

- All this leads to a selected few which have the potential to become the next “Beyond Meat”, including IPO, including higher valuations. But the much larger total market share will be occupied by these “new food” family businesses, which are also critical for sustaining the multiple market “disruptions”, and which are purely profit-orientated, not out for revenues, and thus are not that interesting for VCs because of the lack of “phantasy” (high valuations), but rather for strategic/conservative investors like family offices, corporates, or pension funds.

- "We shouldn’t forget that these companies have brought to the market a significant number of food innovations. Hence, one may find their growth strategy aggressive, but we can’t ignore the fact they are bringing very attractive innovations to the market. That being said, the size of a round is all about what a start-up needs to execute its growth plan. Some food start-ups evolve in a winner-takes-all market and need to raise big to grow first and fast. Some food start-ups evolve in a capex-intensive context and need to raise big to execute, especially in this industry where factories and capital expenditures are often at stake. In these examples, it is just normal that food start-ups raise substantial rounds. On top of this, more recently, some start-ups launched rounds feeling the urge of raising before capital withdraw. We did not perceive this as a sign of aggressivity but prudence from the entrepreneurs".

- "It is very useful that some VCs can finance start-ups in their young years, when profitability is a distant horizon. VCs are thus filling a gap left by banks focusing on profitable companies. However, it is reasonable to assume that a stronger focus will be put on profitability, even if we are fully aware breakeven will be harder to reach as inflation and labour shortage still represent burdens for the industry. First, because start-ups with positive unit economics have a higher probability of survival. Second, because start-ups with a close profitability horizon will probably be sold with a premium. And last, because companies with profitable horizon are eligible to LBOs strategy, hence opening new exit doors for VCs funds.

- "Without any doubts, the FoodTech VC industry has experienced a setback in activity in Q1’22. On one hand, COVID did hit massively the food supply chain encouraging massive investments to support innovation and disruption in consumption habits, at a faster pace. This frenetic pace has enabled quicker adoption from consumers to digital native brands, encouraged people to shift diet towards more plant-based food and finally accelerated considerably the adoption for certain new tech, such as on-demand food business; thus, driving rounds and valuations significantly upwards. On the other hand, the European economic context now advises caution. We are almost behind post-covid consumption boom, covid subsidies and debt facilities from governments are coming to an end, war in Ukraine is bringing uncertainty on top of pandemic wide-open wounds and global inflation is a running train. There might be some changes in VCs strategy. Some obvious changes that we forecast are premium on deals with a good capital efficiency ratio (level of revenues over how much a company has raised) or premium on deals close to rentability".

- "Foodtech is an umbrella term that gets a number of odd disciplines under the same roof. The vast majority of investment has been attracted to Delivery and Plant-Based, effectively driving increased valuations and a large investment pool that is now under question. I personally feel this questioning was actually there even before the current market turmoil; as investment was allocated to companies that struggle to reach profitability despite revenue growth (delivery) and lack of consumer support on a global basis (plant based). We believe the agrifood market is much needed for disruptive innovation in order to increase sustainability and efficiency, and there are a large number of categories where startups are developing technology and intellectual property that is definitively needed by the industry. And Technology, Intellectual Property, Industrial Property are the key elements to take into account when valuing or comparing startups, avoiding inflationary rounds and basing the process on solid market positions".

- "At Eatable Adventures we focus on Early stage ventures, profitability is almost impossible to reach at this phase. Revenue is the driver for early stage, demonstrating growing momentum and customers love for the products or services the startup provides is the best showcase to attract investors and clients. More mature startups definitively shall look for profitability as soon as possible in their lifecycle".

- "Hyper valuation will eventually occur in one or another vertical, is something hard to avoid; investment momentum attracts new ventures willing to make a dent and also investors willing to participate in promising market segments. Therefore this inflation may happen again. On the other hand, Agrifood R&D is very much underserved, and the need to identify, create and get to market a host of novel Biotech and IT solutions to serve what is one of the largest market segments on earth will just grow in the future".

Antonio Iannone